Research shows millennials need experience, not just education, in finance

LAWRENCE — When the time comes for parents to hand the car keys to their teenager for the first solo drive, they’ve likely spent many hours in the passenger’s seat, teaching about the rules of the road and applying those lessons in real life. In today’s society, however, young people often take the wheel of their financial lives with little to no formal education or hands-on experience. And the financial consequences of lack of education and experience can be just as dangerous.

In “Financial Education is Not Enough: Millennials May Need Financial Capability to Experience Financial Health,” University of Kansas researchers argue that young people benefit from a combination of financial education and the opportunity to apply learning. The study was authored by Terri Friedline, assistant professor of social welfare, and Stacia West, graduate research assistant.

In “Financial Education is Not Enough: Millennials May Need Financial Capability to Experience Financial Health,” University of Kansas researchers argue that young people benefit from a combination of financial education and the opportunity to apply learning. The study was authored by Terri Friedline, assistant professor of social welfare, and Stacia West, graduate research assistant.

The authors received a grant from the FINRA Investor Education Foundation to analyze data from about 6,800 people ages 18-34 from the 2012 National Financial Capability Study.

“There has been plenty of conversation about whether providing opportunities for hands-on, experiential learning would enhance the effectiveness of financial education. We wanted to see if the combination had a stronger association with millennials’ financial health compared to other financial education or hands-on experience alone, or neither,” Friedline said. “We were interested in millennials because they’re coming of age in a tough economic environment, and their financial health of today offers a glimpse into their financial health of tomorrow.”

An executive summary of the research will be released at an event sponsored by New America on Friday, June 5, in Washington, D.C., where a panel of experts will discuss how the findings fit into a broader context of factors influencing financial health for millennials and what the implications are for public policy.

The findings:

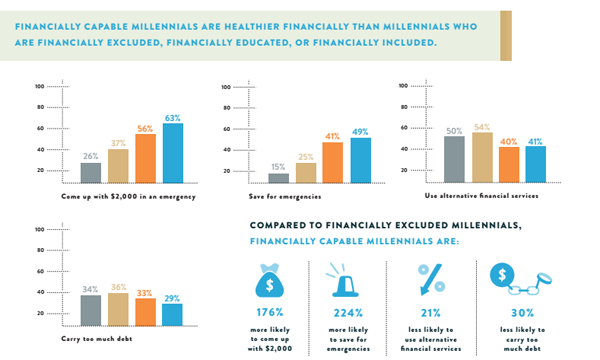

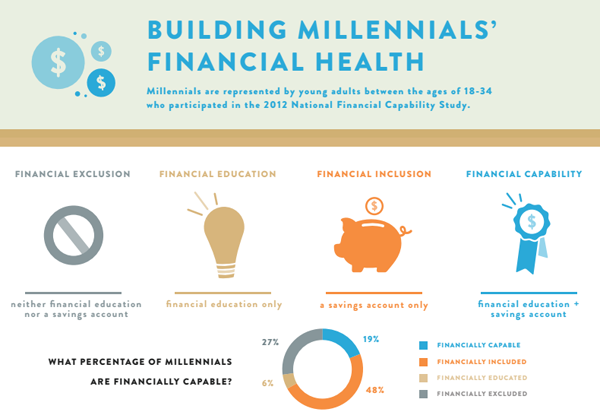

- Nineteen percent of millennials were “financially capable,” meaning they had access to both financial education and some kind of real-life financial experience, such as owning a savings account.

- Six percent were “financially educated” and had received financial education only

- Forty-eight percent were “financially included,” meaning they only had hands-on experience via a savings account

- Twenty-seven percent reported being “financially excluded,” meaning they had neither financial education nor inclusion.

The data showed that compared with financially excluded millennials, those who were financially capable were 176 percent more likely to be able to come up with $2,000 if they had an emergency expense and 224 percent more likely to save for emergencies. They were also 21 percent less likely to use alternative financial services such as payday loans and 30 percent less likely to carry too much debt. Importantly, financial capability was also related to higher financial satisfaction, meaning that financially capable millennials were more likely to be living their preferred financial lives.

The study also showed that financial capability was helpful to low-income millennials, even though only 8 percent were financially capable. While those in the study who earned less than $25,000 annually were less likely to be financially capable, those who did fit that description were significantly more likely to be able to locate $2,000 in an emergency and save for emergencies in advance.

However, compared with their peers without financial education or a savings account, lower-income financially capable millennials were no less likely to use alternative financial services like payday lenders, which can lead to other problems and debt. Although financially capable, lower-income millennials were better off on the whole, their financial capability was not a panacea for solving problems with limited financial resources.

“Unfortunately, for lower-income millennials, financial education and hands-on experience with a savings account are not enough by themselves to avoid using high-cost, high-risk alternative financial services. If there’s no money in the savings account, lower-income millennials may still need to use these alternative financial services to get cash when they need it — even if they’re educated enough to know the financial risks associated with exorbitant interest rates and revolving credit,” Friedline said. “It also illustrates the point that education alone is not enough for millennials to be able to tackle some of the difficult financial decisions they’ll face in life.”

The problems that come with a lack of financial capability are myriad. Young people who did not show financial capability were more likely to carry burdensome debt, which may affect their credit scores and delay their purchase of a home, postpone their saving for retirement, limit their ability to save for their own children’s college education and constrain other investments. Employers are increasingly relying on financial history and credit scores when making hiring decisions as well.

“For financially excluded millennials, all of these things combine to paint a bleak picture of their financial health and how they’re going to be able to make financial decisions in the future,” Friedline said.

Friedline and West have presented the research at the Convening on Financial Capability and Asset Building in St. Louis, sponsored by Washington University’s Center for Social Development, and the University of Maryland Baltimore’s Financial Social Work Initiative. In addition to Friday's event, they will also present the research at the American Marketing Association’s Marketing and Public Policy Conference on Saturday, June 6, in Washington, D.C.

The researchers say addressing the problems outlined in the findings must be at least twofold. Both financial education and opportunities for hands-on experience should be expanded, with schools and other educational institutions offering more financial education and financial institutions offering low-cost checking and savings accounts. These separate efforts can be developed intentionally so they parallel and complement each other.

“Improving young Americans’ financial capability is more important now than ever before. The financial highways that young Americans navigate can be complex and unforgiving,” Friedline said. “And we need to make sure that young Americans have the financial opportunities they need to take control of the wheel and drive their financial health down the roads of their choosing."